Latest update December 16th, 2024 9:00 AM

Oil rich Guyana borrows six times more than last year

…national debt to climb by $79B compared to 2022

Kaieteur News – Although Guyana has been repeatedly advised to keep watch on its ballooning public debt, even as it increases oil production, the Government of Guyana (GoG) believes it has the capacity to take on more loans, thanks to the thriving oil and gas sector.

With a tripling of the country’s Gross Domestic Product (GDP) over the past three years, thanks to oil production – commencing in 2019- the leaders are on route to borrow six times the amount it took in 2022 to fund projects in its national Budget.

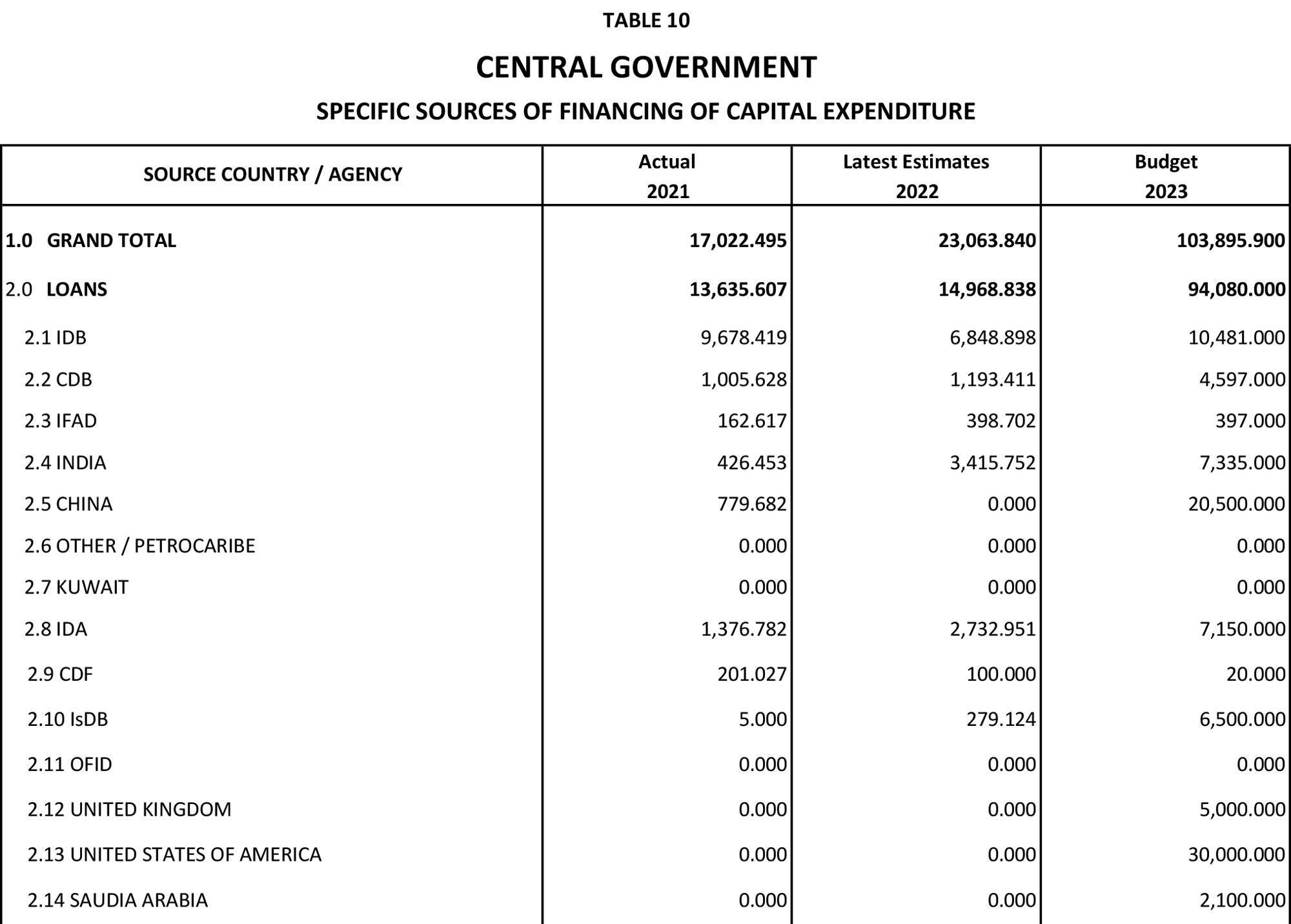

This information is clearly outlined in this year’s Budget documents. Volume One of the Estimates indicate that the latest loan estimates in 2022 was $14,968,838. This year, government plans to borrow a whopping $94,080,000. This amounts to an increase of $79,111,162. It also means that the country’s loans this year to finance capital expenditure is six times greater than the previous year.

Kaieteur News understands that there are 11 creditors the GoG will be engaged with for financing. The list of creditors include the: Inter-American Development Bank (IDB), Caribbean Development Bank (CDB), International Fund for Agricultural Development (IFAD), India, China, International Development Association (IDA), Caricom Development Fund (CDF), Islamic Development Fund (IsDB), United Kingdom, United States of America and Saudi Arabia.

While some of the loans have already been approved and signed, there are loans that are still pending approval. For instance, the loan agreements from the Kingdom of Saudi Arabia were inked on Monday, however government’s application to the US Bank for the Gas-to-Energy project is still pending.

Additionally, it was reported last week that the GoG signed another loan agreement with Qatar to extend the Schoonord to Crane four-lane road to Parika. This loan was not mentioned in this year’s Budget Estimates.

Table in the Ministry of Finance Budget document, depicting the loans Guyana will be adding this year as well as the country’s previous two-year history.

The 2023 Budget was approved in the National Assembly on February 2, to the tune of $781.9 billion. The Ministry of Finance said that a total of US$1.002 billion- approximately GYD$200 billion- from the Natural Resource Fund (NRF) or the oil account will go towards this year’s Budget.

Meanwhile, Budget 2023 indicates that some $9.8 billion in grants from 10 institutions and countries were expected to provide support to Guyana as well. These include the CDB, IDB, Japan, World Bank, China, IFAD, Kuwait, CDF, Global Fund and Germany.

Oil-rich Guyana is among five countries in the Latin America and Caribbean (LAC) Region that were listed as heavily indebted poor countries (HIPC) in an April 2023 report by the International Monetary Fund (IMF).

In the report titled, ‘World Economic Outlook: A Rocky Recovery’, several tables were published showing emerging market and developing economies by Region, net external position, heavily indebted poor countries, and per capita income classification.

Under the LAC table, Guyana along with Bolivia, Haiti, Honduras and Nicaragua were listed as HIPC countries.

Only yesterday it was reported that the GoG inked a new loan agreement with the Kingdom of Saudi Arabia for a US$150 million loan, to develop the housing and infrastructure sectors.

By the end of last year, Guyana’s total stock of public debt increased by 16.9 percent compared to 2021. It was the Finance Minister, Dr. Ashni Singh who said during the Budget presentation that the nation was US$3.654 billion in debt.

It must be noted that during this year’s Energy Conference hosted in February, the Finance Minister announced to the international audience that Guyana is now in a better position to take more loans as the country’s Gross Domestic Product (GDP) has tripled in the last three years.

Dr. Singh said Guyana has been able to prudently manage and reduce the debt to GDP ratio over the past 30 years. He explained, “Those of you who have been following Guyana for long enough, would know that there was a period just about maybe 30 years ago when Guyana’s public debt to GDP exceeded six times the size of the economy. In 1991/ 1992 the public debt to GDP ratio exceeded 600%…we have been able over the years to bring public debt down and today Guyana’s public debt to GDP ratio stands at 24.6 percent.”

The Finance Minister paused his presentation as he received a resounding applause for the progress the country made in lowering its debt to GDP rate. He however went straight into his point that this means Guyana is now in a better position to take more loans. “I didn’t put a chart up with international comparators but if you; I mean many of you are familiar with these numbers around the World. You will no doubt recognise that the debt to GDP ratio of 24.6% in fact places Guyana ahead of almost every economy, certainly in this hemisphere and puts us in a position where we actually have fairly significant head room to borrow,” he shared.

Former Auditor General, Anand Goolsarran had warned that while Guyana’s medium-term economic prospects appear very favourable due to anticipated oil revenues, government should nevertheless exercise restraint in spending, given the volatility of oil prices. Goolsarran had made the comments in his Column, published in the Stabroek News.

Opposition Member of Parliament (MP) Volda Lawrence and former Health Minister during this year’s Budget Debates expressed worry over the nation’s growing public debt. She said that the country was falling into a dangerous trap, quite similar to the one that ensnared oil-producing states like Nigeria and Ghana.

She told the House, “Sir, the government’s eschewing the use of the burgeoning natural resource funds, in preference to borrowing from any and all sources, on the assumption that oil prices will remain high, thus allowing easy repayment of loans taken today, is falling into the same trap as did Ghana and Nigeria, for example.”

Lawrence pointed out that external public has grown steadily since the People’s Progressive Party (PPP) took office in August 2020. The figure ballooned from US$1.321 billion in 2020 to a projected US$2.146 billion in 2023, or 62% she flagged.

As such, she noted, “Any collapse in oil prices Mr. Speaker, will leave the country dangerously exposed to situations not unlike what happened to Sri Lanka and Uganda.”

Lessons from Ghana

Kaieteur News reported that oil-rich Ghana was dubbed fastest growing economy on earth in 2019, but now that African nation is drowning in debt.

The glory days of Ghana’s offshore oil operations can be traced back to December 2010. The West African nation began pumping oil from its first commercial discovery in its Jubilee Field. Those operations delivered US$1B in earnings annually to the State.

Nine years later (in 2019), Ghana was dubbed to have the fastest-growing economy. It was also praised for the steps it took to improve the regulation of the industry. In fact, Ghana was seen as a champion of growth for other nations within the continent and further afield to follow.

But in a matter of three years, this glimmering picture of marvelous economic management was unexpectedly obliterated. Ghana moved from riding a wave of meteoric growth to now wallowing in the abyss of indebtedness. From 2019 to 2022, the country that was once paired with Guyana as a model state on good governance is now a lesson on the perils of the oil curse.

International media reports released in December 2022 said Ghana is in such a worrying state of debt distress, that it has been forced to suspend payments on most of its external debt. In fact, its Finance Ministry said it will not service selected external debts including its Eurobonds, commercial loans and most bilateral loans.

Ghana’s Ministry said, “Ghana is today faced with major economic and financial crisis and its attendant social challenges. In 2020 and 2021, the Covid-19 pandemic negatively impacted our fiscal and economic situation. Global risk aversion triggered large capital outflows, a loss of external market access and rising domestic borrowing costs.”

Nigeria drowning in debt

Similarly, after more than six decades producing oil, Nigeria, thanks to the decisions of its politicians, is drowning in US$108B of debt.

But in order to survive the dreaded COVID-19 pandemic, Africa’s biggest oil producer needs US$11B in fresh loans from financial institutions such as the International Monetary Fund and the World Bank to purchase basic medical and food supplies.

In 2021, this newspaper reported that some financial institutions are hesitant to provide the African nation of more than 200 million people with more loans due to rampant corruption by politicians.

Be that as it may, the Natural Resource Governance Institute (NRGI) which is closely following the crisis in Nigeria opined in one of its analytical pieces that oil-rich countries such as Nigeria have clearly found themselves stuck between the “rock” of economic ruin and the “hot place” of environmental catastrophe.

But NRGI, one of the world’s leading non-profit organisations in improving countries’ governance over their natural resources, firmly believes that all is not lost for Nigeria. It posits that the future of Nigeria lies in weaning itself off of fossil fuels and preparing its economy for the energy transition that is taking place the world over.

The Institute was keen to note that some countries which are rich in oil are already headed in the wrong direction. In this regard, it noted that politicians in some countries are intent on proving that their country can become a world-class profit-making machine, just as international oil companies did in the 20th century. It warned however, such lofty dreams come at a price.

NRGI said, “The difficulty of navigating transition is hardly exclusive to Nigeria… From Mexico to Mongolia, from Ghana to Guyana, governments must address the unknown future of energy markets. As the world recovers from the pandemic and continues to transition toward renewable energy, city skies may remain relatively clear. But how resource-producing countries manage the decline in fossil fuels is critical, especially after the shock of the economic and health crisis.”

Similar Articles

THE BLUNT OF THE DAY

Sports

Features/Columnists

Exporters are being left to fend for themselves

Exporters are beIng left to fend for themselves Peeping Tom… Kaieteur News- Vice President Bharrat Jagdeo has a new... more

Let the asylum seekers go: a first step for Venezuela to rebuild relations in the Americas

By Sir Ronald Sanders Kaieteur News – The government of Nicolás Maduro in Venezuela has steadfast support from many... more

Weekend Cartoon