Latest update March 28th, 2025 1:00 AM

Latest News

- “It will be a very bad day for Venezuelan if they attack Guyana or ExxonMobil”—Rubio declares

- Guyana gets info on U.S. tax evasion allegations against Mohameds, Mae Thomas

- US$35 injected into banking system to address foreign currency shortage—VP Jagdeo

- Citizens to stage protest today against lack of access to information in Guyana

- Guyana vows to stand with U.S.

An Analysis GBTI’s Financial Performance for 2017

Dear Editor,

Dear Editor,

The Guyana Bank for Trade & Industry Limited’s annual report for their financial year ended 2017 was recently made available to its shareholders. The Bank has been marred in several controversial legal matters involving the Special Organized Crime Unit (SOCU) coupled with a massive fraud close to $1 billion that occurred in 2017.

This missive sought to thoroughly dissect and or analyze the financial health of the institution in the interest of all of its shareholders including both majority and minority; and other key stakeholders.

Commercial banks and all other licensed financial institutions are governed by the Financial Institutions Act 1995 which is enforced, inter alia, by the central bank. The Central Bank has the supervisory and regulatory authority for these institutions and by extension the financial sector.

While it is noted in the annual report that the reporting is subject to two reporting standards – that is, the IFRS and the Bank of Guyana Supervision Guideline No.5, logically the central bank which is the regulatory and supervisory authority ought to be and is the supreme authority in this regard.

The revenue streams of a bank constitutes four key components – (1) commissions and fees; (2) investments in financial instruments both locally and abroad; (3) interest received from loans and advances and; (4) foreign exchange.

The main income or the larger portion of its income, however, is earned from the loans and advances or its credit portfolio. Thus, it is this component that when perusing a bank’s balance sheet, it is prudent to examine the asset quality of the bank’s balance sheet.

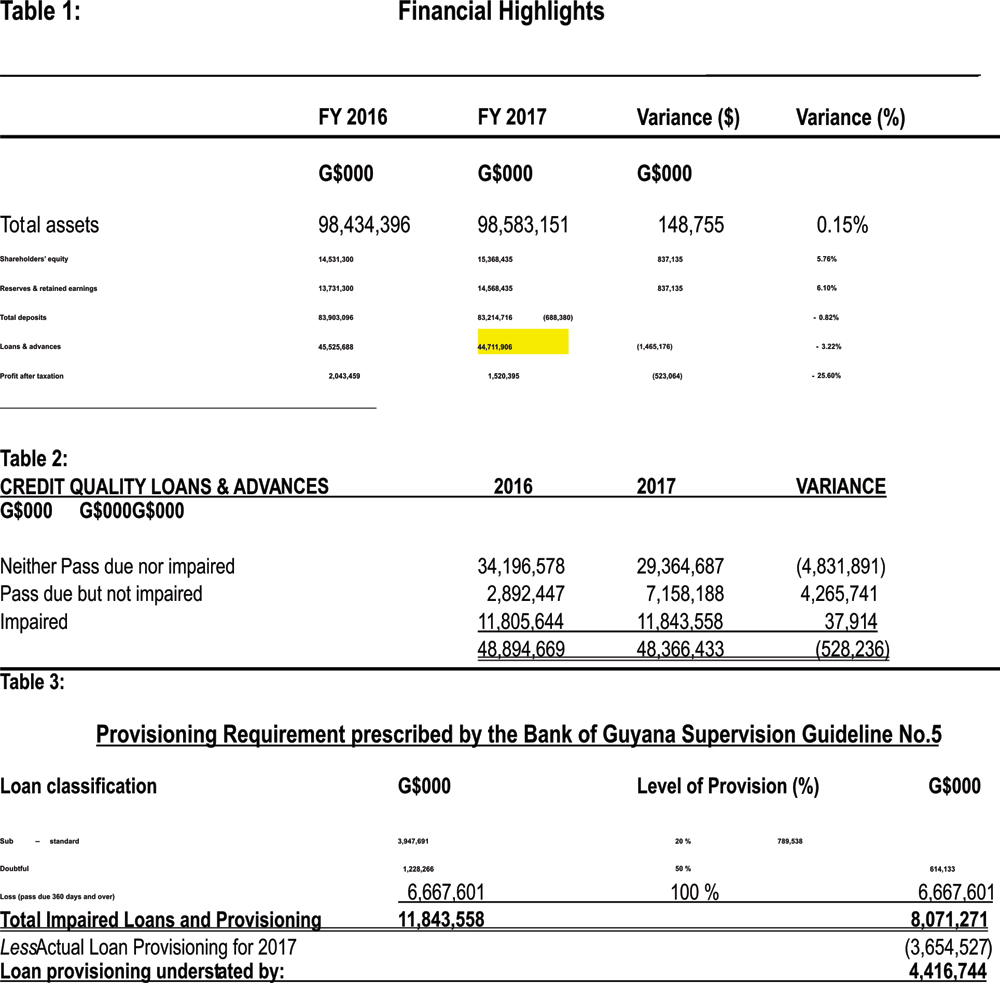

The bank has reported an after tax profit of $1.5 billion for 2017, down from $2 billion in 2016 or by 25 percent while total assets increased marginally by 0.15 % or $148 million compared to the corresponding period in 2016; retained earnings and reserve increased by $837 million or six percent from $13.7 billion in 2016; net loans and advances declined by $1.4 billion in 2017 or 3.22 % from $45.5 billion in 2016 to $44 billion in 2017.

As can be deduced from the tables above, the bank has reported a net loans and advances in its balance sheet of $44.7 billion out of a total loan portfolio of $48.3 billion thereby reflecting a loan provisioning of $3.6B. However, of extreme importance, the level of non-performing loans is a whopping $11.8 billion representing 24.5 percent of its total portfolio and, more worryingly the bank has underprovided for these bad loans by a massive $4.4 billion as is illustrated in the above table and prescribed by the regulatory guidelines.

This means that the profits declared are not real profit. Additionally, this practice is referred to as creative accounting or sometimes referred to as ‘window dressing’ – an accounting terminology which accountants and students of accounting would know that it is just a decent term in the accounting profession to describe in essence – management fraud.

As a comparison to further illustrate how GBTI’s financial health is deteriorating at a rather rapid pace, GBTI’s financial performance was once the most financially sound and enviable bank in Guyana. To this end, having perused the annual report for the financial year 2008, the bank had reported a profit after tax of $940M, a net loan portfolio of $12.8 billion and reserves and retained earnings of $3.85 billion.

Of interest to note, in that year the level of impaired or non-performing loans stood at $1.851 billion and a total provisioning of $1.9 billion; clearly reflecting that the provisioning for bad loans was actually more than the level of the bad loan portfolio. When re-worked to compute what the actual level of provisioning should be as prescribed by the Central Bank’s Supervision Guideline No.5, that figure worked out to $1.4 billion.

Again, this was a another reflection of prudent financial management of the institution and also skillfully declaring less profits by providing more for bad loans rather than declaring more profits and paying more corporate taxes. In other words, the bank was actually making more profits in those years up to 2009.

From then on, the bank started to weaken at a rather alarming rate through excessive risk taking, and poor quality lending practices. It is in the interest of the 40% minority shareholders, against the background of the analyses presented in this letter, to effectively and objectively ask the right questions and grill the Board of Directors at the next AGM set for June 21, 2018.

Yours sincerely,

Banking and Economic Analyst

MSc. (Banking)

(Name & Address Supplied)

Similar Articles

THE BLUNT OF THE DAY

Sports

Features/Columnists

The PPP has started the intimidation

Peeping Tom… Kaieteur News- In politics, as in life, what goes around comes around. The People’s Progressive Party/Civic... more

The Caribbean: Destined to Grin and Bear the Consequences of Its Self-Created Vulnerabilities?

By Sir Ronald Sanders For decades, many Caribbean nations have grappled with dependence on a small number of powerful countries... more

Weekend Cartoon